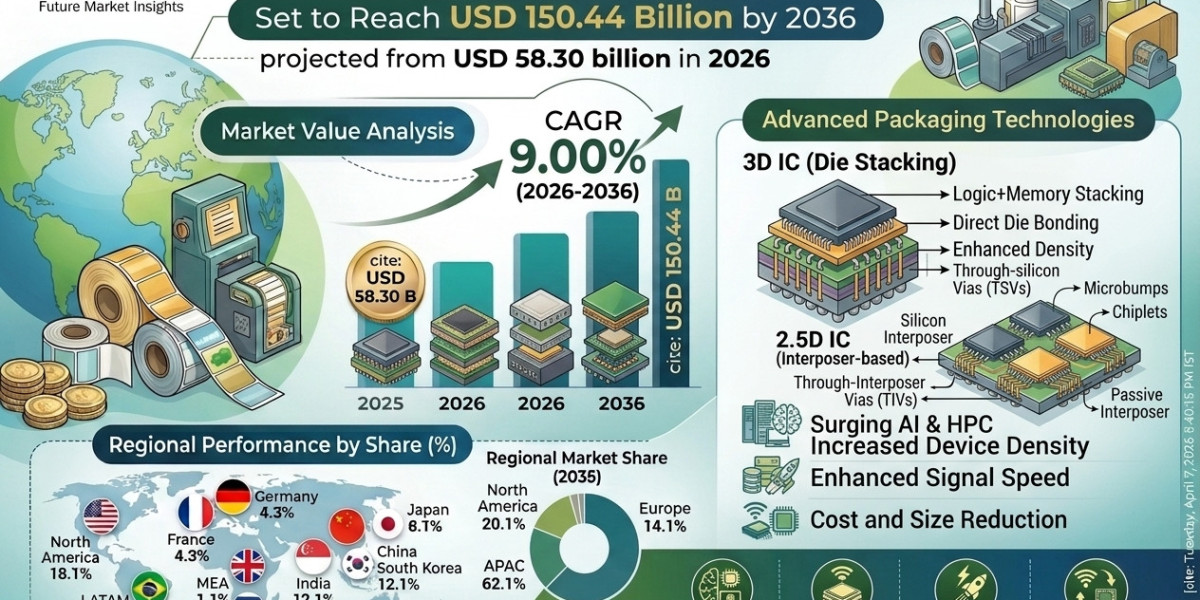

The global 3D IC and 2.5D IC Packaging Market is projected to grow from USD 58.3 billion in 2025 to USD 138.0 billion by 2035, registering a strong CAGR of 9.0%. The market is expected to add USD 79.7 billion in absolute growth, reflecting the rapid evolution of semiconductor packaging as a critical enabler of advanced computing systems.

Market Snapshot: Key Highlights

- Market Value (2025): USD 58.3 billion

- Forecast Value (2035): USD 138.0 billion

- Absolute Growth: USD 79.7 billion

- CAGR (2025–2035): 9.0%

- Leading Technology: 3D TSV (50.6%)

- Leading Application: Logic (45.9%)

- Leading End Use: Consumer Electronics (38.4%)

Key Companies:

TSMC, Intel Corporation, Samsung Electronics, Amkor Technology, Advanced Semiconductor Engineering, Broadcom

Market Overview

The 3D IC and 2.5D IC packaging market is undergoing a transformational shift, moving from traditional chip packaging to advanced heterogeneous integration. These technologies enable:

- Stacking of multiple chips (logic, memory, sensors)

- Higher bandwidth and faster data transfer

- Reduced power consumption and latency

- Compact and efficient device designs

They are now essential for AI, cloud computing, 5G, and automotive electronics.

Growth Trajectory Analysis

2025–2029: Foundation Phase

- Market grows from USD 58.3 billion to USD 75.5 billion

- Driven by:

- TSV technology improvements

- Yield optimization

- Early adoption in high-performance computing

2030–2035: Acceleration Phase

- Market reaches USD 138.0 billion

- Adds USD 48.3 billion in this phase alone

- Driven by:

- Chiplet architecture scaling

- AI and edge computing demand

- Automotive and 5G applications

Why is the Market Growing?

Demand for High-Performance Computing (HPC)

HPC and data centers account for the largest share (~38%), driven by:

- AI training workloads

- Cloud computing

- Simulation and analytics

Advanced packaging enables:

- Faster memory access

- High bandwidth

- Reduced latency

Growth in Consumer Electronics

Consumer electronics contribute ~25% of demand, including:

- Smartphones

- Wearables

- AR/VR devices

3D and 2.5D packaging allows:

- Smaller form factors

- Improved performance

- Better thermal efficiency

Automotive and ADAS Expansion

Automotive accounts for ~15% share, driven by:

- Autonomous driving systems

- Advanced driver assistance systems (ADAS)

- Infotainment platforms

These applications require:

- High computational power

- Reliability under harsh conditions

Get Access of Research Report Sample: https://www.futuremarketinsights.com/reports/sample/rep-gb-25260

5G and Networking Infrastructure

- Accounts for ~12% of market

- Requires:

- High-speed interconnects

- Low latency

- Compact designs

Technology Insights

3D TSV Dominates (50.6%)

Through-Silicon Via (TSV) technology leads due to:

- High-density vertical integration

- Shorter interconnect distances

- Improved signal performance

It enables seamless integration of:

- Logic + memory

- Multi-chip architectures

Application Insights

Logic Segment Leads (45.9%)

Logic chips dominate due to:

- Increasing processor complexity

- Demand for faster computing

- Integration with memory

Used in:

- CPUs and GPUs

- AI accelerators

- Mobile processors

End-Use Insights

Consumer Electronics Leads (38.4%)

Driven by:

- Miniaturization requirements

- Performance expectations

- Rapid product innovation cycles

Key Market Trends

Shift Toward Chiplet Architecture

Companies are moving from monolithic chips to:

- Modular chiplets

- Interposer-based designs

- Scalable integration

Rise of AI and Data-Driven Applications

AI workloads require:

- High memory bandwidth

- Fast processing

- Efficient packaging

Advanced Thermal Management

Innovations focus on:

- Heat dissipation

- Power efficiency

- Reliability in dense packaging

Ecosystem Collaboration

Partnerships between:

- Foundries

- OSAT providers

- Chip designers

are accelerating innovation and scalability.

Market Challenges

High Cost and Yield Issues

- TSV fabrication complexity

- Yield losses increase costs

- Advanced testing requirements

Supply Chain Dependencies

- Reliance on advanced fabs

- Geopolitical risks

- Material shortages

Technical Complexity

- Integration challenges

- Thermal management issues

- Design compatibility constraints

Regional Insights

Asia-Pacific Leads Growth

- China: 12.2% CAGR

- India: 11.3% CAGR

Driven by:

- Government semiconductor initiatives

- Manufacturing expansion

- Consumer electronics demand

Europe

- Focus on automotive and industrial applications

- Strong R&D ecosystem